Current Market Data

U.S. government data shows builders increased the pace of single-family home construction while slowing the pace of multifamily starts.

The National Association of Home Builders/Wells Fargo Housing Market Index rose for the fourth month in a row in April as the construction industry remained “cautiously optimistic.”

Last year, inventory supply was 185.7% lower at less than one month.

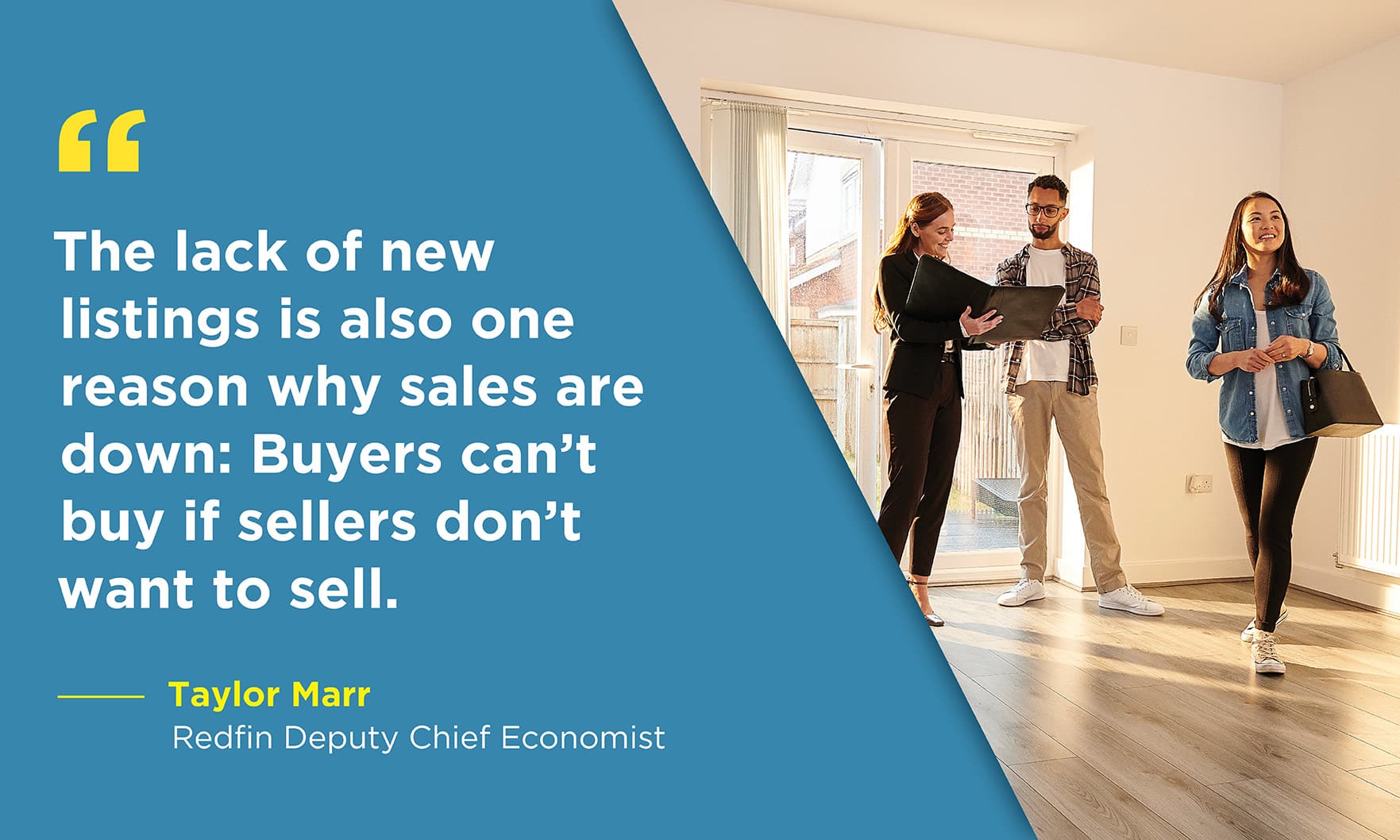

New listings are still in short supply, falling 21.8% from last year.

This was the fourth week in a row of declines, leaving prospective buyers hopeful for sustained low rates throughout spring homebuying season.

One of the best ways sellers can make their home stand out in today’s market is by upgrading their space with luxury renovations and amenities.

Condominium owners looking for more space, access to outdoor areas and increased distance from neighbors often consider a detached home to be a natural upgrade. But are these upsizing dreams actually attainable?

The National Association of REALTORS® Pending Home Sales Index rose for the third month in a row, suggesting the housing market’s contraction could be “coming to an end.”

In Phoenix, home prices were flat year-over-year in January; month over month, they were down 1.2%.

MLS data shows that Phoenix’s median sales price reached $450,000 in February 2022. A year later, that price dropped 7.8% to $415,000.

The supply of new homes for sale ticked lower from February, according to government figures.

The annual rate of 4.58 million sales was up 14.5% from January but down 22.6% from the February 2022 rate of 5.92 million.

Nationally, the week of April 16-22 is likely to provide sellers with the most favorable conditions for a successful sale of any week of the year, although the exact timing varies widely by market.

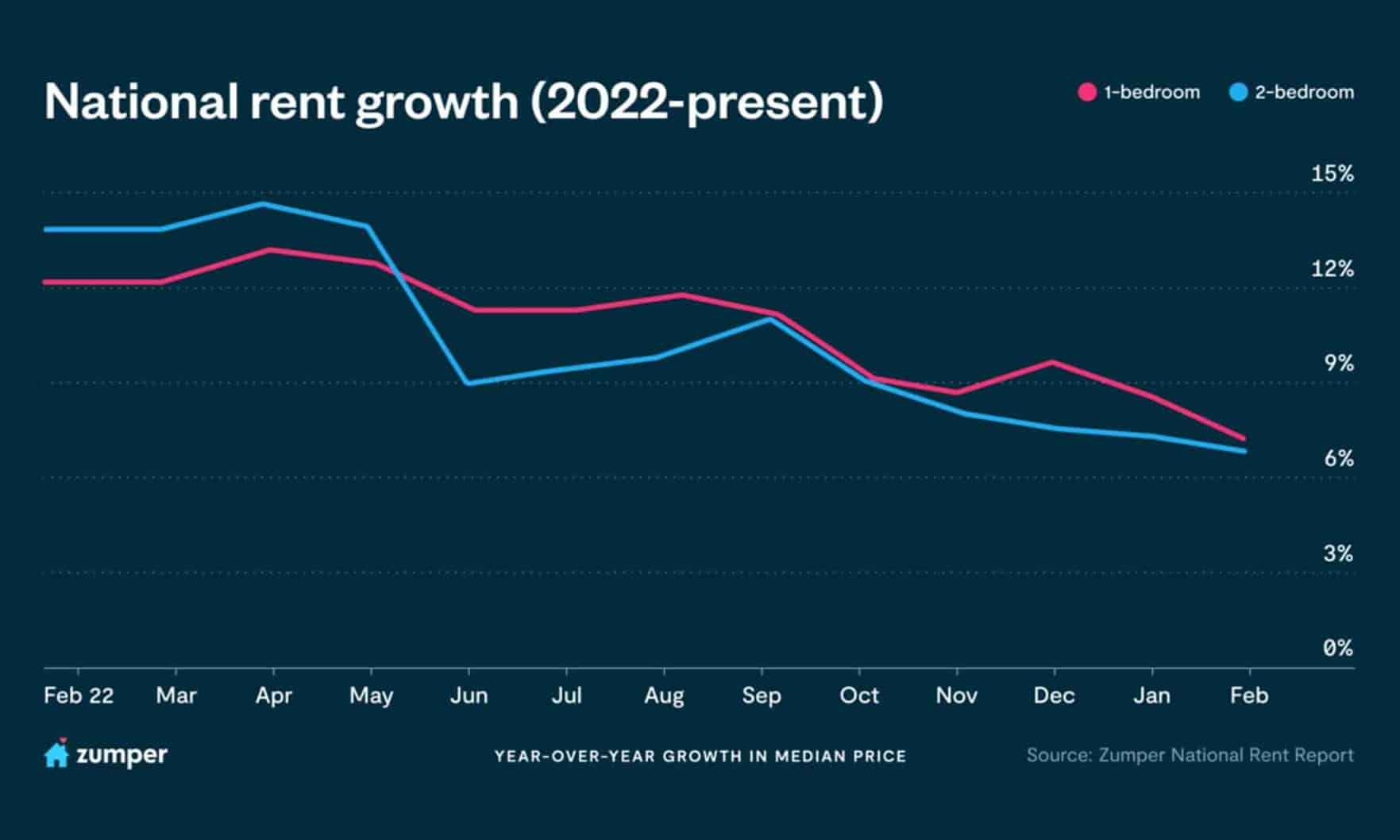

Month-over-month increases in rental costs have slowed across the country, but it’s still more expensive to rent a one- or two-bedroom apartment in Phoenix than it was last year.

A shortage of existing-home inventory is driving more people to the market for newly built homes.

Increased mortgage rates have sidelined many would-be buyers, allowing inventory levels to increase. As a result, buyers can now “shop around” more than during the peak of the pandemic, putting the burden of concessions back on sellers.